Waypoint No. 1: The Seven-Year Tax Window That Closes at 73

Waypoint

No. 1 · May 2026

A Shetland Financial Publication

Welcome to the first issue of Waypoint. As we mentioned in recent weeks, we are stepping back from weekly market commentary and toward something more useful: twice-monthly notes on the tax and planning decisions that actually move the needle. Our first issues covers Roth conversions.

The Seven-Year Tax Window That Closes at 73

Most people retire, breathe a sigh of relief, and assume the hard tax planning is behind them. In reality, the years between retirement and age 73 are often the most important tax planning years of an entire lifetime. This is the Roth conversion window, and it closes the moment Required Minimum Distributions begin.

Many retirees who stop working at ~65 have a common tax situation. Earned income stops. Social Security may not have started yet, or is being deliberately delayed to age 70. Pre-tax IRA and 401(k) balances are sitting untouched, growing every year. For a brief period, taxable income drops into a bracket the retiree has not seen in decades. Then at age 73, RMDs begin, Social Security is in full swing, and suddenly that same retiree is back in a 24 or 32 percent bracket, often for the rest of their life. The window was open. Most people did not know to use it.

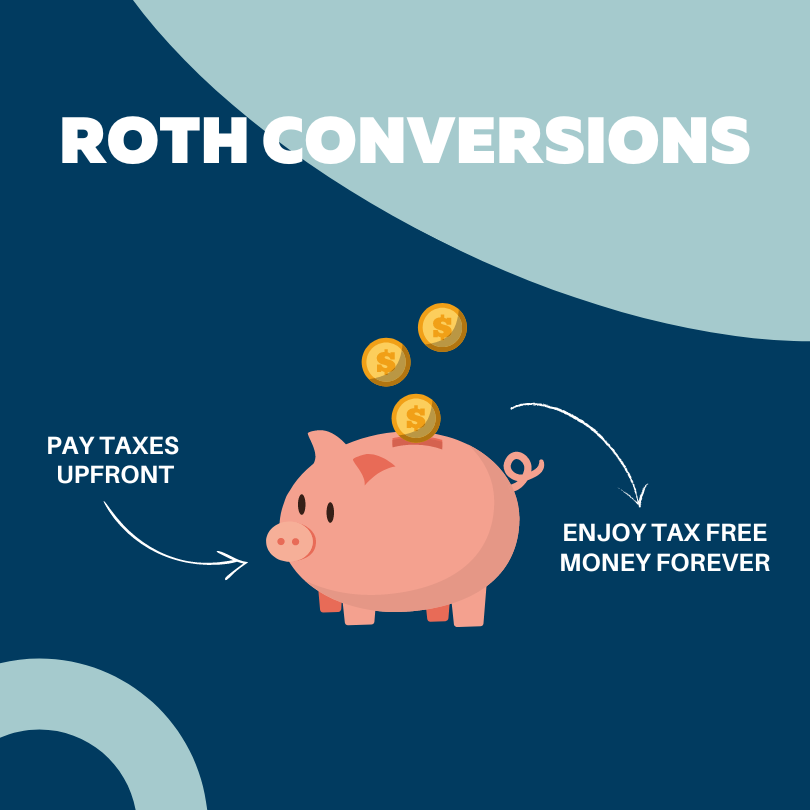

A Roth conversion is the strategy that uses this window. You voluntarily move a portion of a traditional IRA or 401(k) into a Roth IRA, pay the tax today at the lower rate, and from that point forward the assets grow tax-free, come out tax-free, and are not subject to RMDs. Done thoughtfully across multiple years, a retiree can deliberately fill the 12 or 22 percent brackets while they are available, rather than being forced into higher brackets later when income sources stack on top of each other.

The tax-rate angle is only part of the value. Roth IRAs have no RMDs during the original owner’s lifetime, which means the account can keep compounding tax-free for as long as the retiree wants to leave it alone. That same feature makes Roth assets one of the most powerful estate planning tools available today. Under current law, non-spouse beneficiaries must drain inherited retirement accounts within ten years. If those assets are pre-tax, the heirs receive a ten-year tax bill on top of their own peak earning years. If those assets are Roth, the heirs receive ten years of continued tax-free growth followed by tax-free distributions. The difference, on a meaningful balance, is often six figures of family wealth.

The reason most retirees miss this window is not complexity. It is coordination. A financial advisor managing the portfolio is usually not the person preparing the tax return. The CPA preparing the return sees the result of last year’s decisions, not the projection of next year’s brackets. Roth conversions only work when someone is looking at projected taxable income, current bracket capacity, IRMAA thresholds, state tax impact, and long-term portfolio strategy at the same time. That is a multi-year, multi-discipline analysis, and it cannot be done in a one-hour annual review.

This is the kind of planning Shetland was built to do. Tax preparation, financial planning, and investment management sit on the same desk, with the same person looking at all of it. If you are between 60 and 72, or you have a parent or family member who is, it is worth a conversation before another year of the window closes. Reply to this email or call the office and we will run the numbers.

As always, thank you for reading.

Kevin Dodgson CPA, CFA, CFP®

Founder & CEO, Shetland Financial