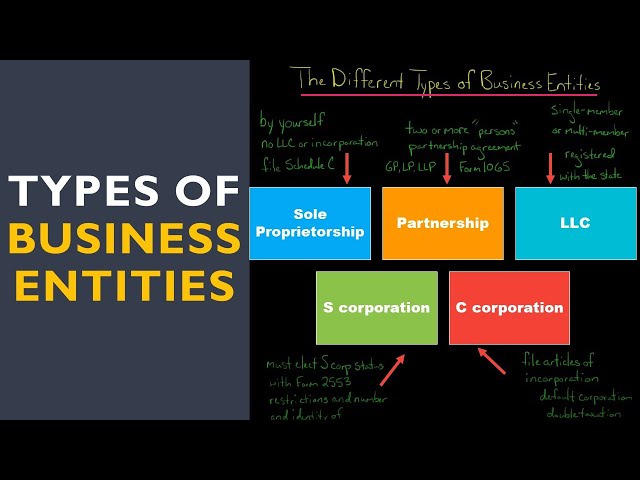

One of the most common questions I get from people who are thinking about starting their new business is how they should set up their business. So let’s walk through some of the various options and which legal entity is right for your new business.

Sole Proprietor

This is technically one of your options, but it’s more accurate to say it’s what happens if you don’t decide to do something else. That’s because the IRS treats you as a sole proprietor if you make any business income and haven’t told them to treat you otherwise.

Legal Issues

The biggest downside to being a sole proprietor is that because your business is not a separate legal entity, you are personally liable for everything the business does. If an unhappy customer or vendor sues you for a million dollars, you might lose your life savings.

You do not need to file any paperwork to be a sole proprietor, but you might still need a business license to operate a business. Check with your local town government to find out. If you’re operating a professional service you also might need a state license.

Taxes

Since this is not a separate legal entity, for tax purposes all income you make from your business will be on your personal tax return (Form 1040 – Schedule C). You will list all your revenue and expenses on Schedule C and the net profit is what you’ll pay taxes on. Remember, you’ll pay both income tax AND self-employment taxes on your profits.

Partnership

If you decide to go into business with someone else, you can form a partnership to split the startup costs and share in the profits. You can have as many partners as you want and can agree to structure it however works best for you.

Legal Issues

When you form a partnership, the most important document is what’s called a “Partnership Agreement”. This basically spells out exactly how you’re going to allocate the costs and eventual profits of the business, as well as who gets to make final decisions or how voting rights will be determined. Sometimes these can be very simple: you and your friend each put up $5,000 and agree to split everything 50/50.

These agreements can also be more complex: you and your friend decide to open a restaurant, but since you have all the experience, the friend puts up all of the startup costs and you agree to manage the day-to-day business. At the end of the year, you still agree to split profits equally. You can also agree to split up costs unequally: investor A puts up $20,000 and investors B and C each put up $2,000. It’s up to you how you want to structure any deal – just make sure to put it in writing.

One of the downsides of a partnership is legal liability. As a partner, you’ll be responsible for the debts and obligations of the partnership as if you personally signed for them yourself. If your partner takes out a giant loan, the partnership as a whole is responsible for paying it back (even you).

*Note: since we’re discussing setting up a business, we’re speaking here about ‘General Partnerships’ where each partner has a hand in running the business. There is a separate investment structure known as a “Limited Partnership” that limits your exposure to this risk, but you can’t actually make any decisions as a limited partner. You’re essentially just an investor.

Taxes

A partnership is what is regarded as a “pass-through entity,” which means that its profits are not actually taxed – the amounts are simply passed through and taxes are paid on your personal return.

As a separate legal entity, a partnership will file its own tax return (Form 1065). This return will show the total revenue and expenses for the partnership as a whole. When this is completed, each individual partner will receive a form (Form K-1) showing what their share of the profits was. This info is used to populate your individual tax return, and you’ll pay taxes on those amounts at your personal tax rates.

Limited Liability Company (LLC)

LLC businesses have become incredibly popular in the United States, and for good reason. They generally combine the favorable tax treatments from the above options while eliminating the legal liability issues.

Legal Issues

An LLC is a separate legal entity. It can open its own bank accounts and have its own contracts with customers and vendors. It can even own real estate. This also means that someone could hypothetically sue your LLC for a million dollars and bankrupt the business – but just the business. Your personal savings (other than what you invested in the business) are safe. This limited liability is one of the main appeals of setting up an LLC.

One drawback of creating a separate legal entity is that it doesn’t come free. LLCs are created by filing paperwork with the state. The forms are generally fairly simple, but the fees can vary (currently $50 in some states, all the way up to $500 in Massachusetts – which would be where my own LLC is incorporated). You’ll also need to file Annual Reports and pay the fees annually thereafter.

Taxes

Depending on if the LLC has one owner or multiple owners, for tax purposes it is simply treated as a sole proprietor or partnership. If you’re the only owner (known as a “Single Member LLC”, or SMLLC), all of the income and expenses from the business will be reported on your personal tax return on Schedule C. If there are multiple owners, your LLC will file a Form 1065 as if it was a partnership, and each owner will receive a K-1 to use to fill out their own return.

S-Corp

An S-Corporation is a type of corporation that follows specific rules regarding how many members you have and who those members are.

Legal Issues

Similar to an LLC and Partnership, an S-Corp is a separate legal entity. It is created by filing paperwork with the state and paying the required fees. As a corporation, its owners are shareholders and the company can assign shares however it chooses. However, by law, it cannot have more than 100 shareholders and there can only be one class of stock (ie, no “A-shares” and “B-shares” to give certain people more power). All of the shareholders must be individuals, not other corporations or partnerships – you can’t have an S-corp own another S-corp.

Taxes

An S-corp files a corporate tax return (Form 1120S). The amounts on this return are then passed on to each shareholder through a K-1, similar to a partnership. You’ll receive a K-1 even if you’re the only shareholder of the business.

C-Corp

A C-corporation, usually just referred to as a “corporation”, is the business structure you’re probably most familiar with – basically every large company is set up this way.

Legal Issues

A corporation is a legal entity that is owned by shareholders. Unlike an S-corp, a C-corp can have as many different shareholders as it wants, can have as many classes of stock as it wants, and can be owned by non-individuals.

Taxes

Unlike the other entities we’ve discussed, a C-corp is NOT a pass-through entity. Profits are taxed at the entity level before shareholders even touch them. Currently, 21% of net profits are taxed at the corporate level, and the remaining profits then continue to sit in the business bank accounts. If the corporation decides to return that money to the shareholders as a dividend, that money is also taxed on the shareholder’s personal tax return. This is what’s known as “double-taxation” and is the reason that financially speaking it doesn’t make sense for most small business owners to set up their company as a C-corporation.

Summary

So which entity is right for you? As a general rule, setting up an LLC winds up being the best choice for most new small business owners, due to its limited legal liability and tax treatment. But the right choice for you could be different, so reach out to a qualified tax advisor or attorney if you need help.