Waypoint No. 3: Mid-Year Tax Check-In

Mid-Year Tax Check-In: 5 Moves Before June 30

Most people don’t think about taxes until April. But if you wait that long, many of your best opportunities are already gone. The window between now and June 30 is one of the most valuable, and most overlooked, moments in your financial year. Half the year has unfolded, so you have real numbers to work with. And half the year remains, so you still have time to do something about it. Here are five moves worth considering before that window closes.

1. Make Sure Your Tax Payments Match Your Reality

If your income this year looks different from last year (a bonus, a business distribution, the sale of an investment, a job change), your tax payments may no longer be on track. Underpaying can trigger IRS penalties; overpaying ties up cash you could be putting to work. June 15 is the deadline for second quarter payments. A quick review of your year-to-date income against what you’ve already paid can tell you quickly whether you’re in good shape or whether an adjustment makes sense. If you need help with a quick back of the envelope calculation just let me know.

2. Look at Your Investments for Hidden Tax Savings

The market is up so far this year, but you might not have all winners. If some of your investments have dropped in value this year, those losses can be useful. By selling positions that are down, you can offset gains you’ve already realized elsewhere in your portfolio, potentially reducing what you owe at year-end. This strategy, known as tax-loss harvesting, works best when you do it proactively rather than waiting until December when everyone else is scrambling. At the same time, if you have investments that have grown significantly, now is a good time to think about whether gifting some of that appreciated stock to charity, rather than cash, could generate a meaningful deduction while removing a taxable gain from your picture.

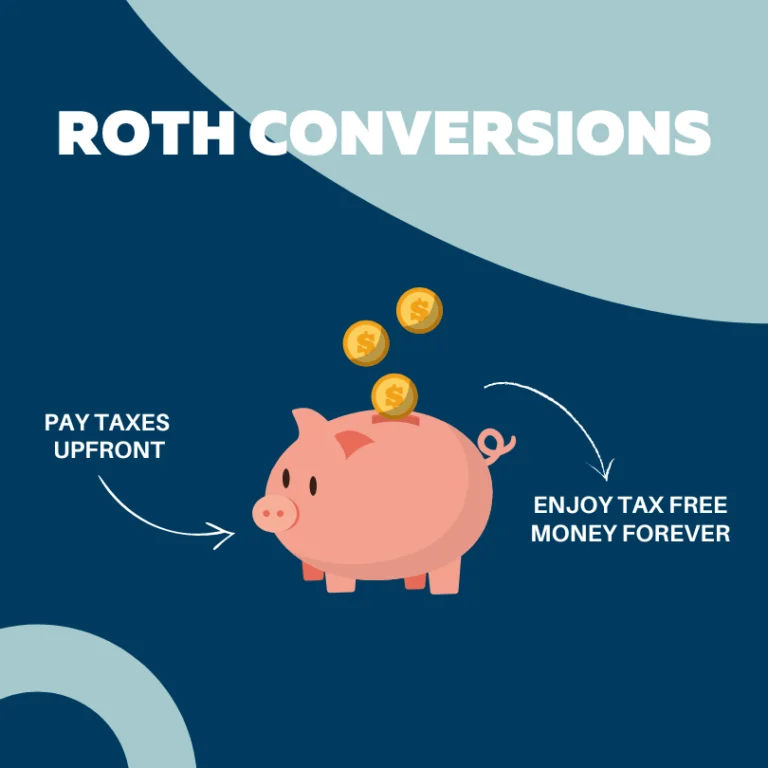

3. Check Whether You’re On Track With Retirement Savings

Retirement contributions are one of the most straightforward ways to reduce your taxable income, but it’s easy to fall behind on pacing, especially if your income fluctuates or you’re self-employed. Mid-year is the right time to see where you stand. If you have a SEP-IRA, Solo 401(k), or profit-sharing plan, your contribution limit is tied to your business income, and June gives you a reasonable sense of what that number will look like. It’s also worth asking whether a Roth conversion might make sense this year. If your income is running lower than usual, converting some traditional IRA assets to a Roth at a lower tax rate can be a powerful long-term move. The best windows are often the ones that pass quietly: a down-income year, a gap before required minimum distributions begin, or any stretch when your bracket dips lower than it will be later.

4. If You Own a Business, Revisit How You Pay Yourself and What You Buy

For business owners, how you structure your compensation can have a significant impact on your tax bill. If you pay yourself through an S-corporation, your salary needs to reflect reasonable compensation for the work you do. Too low can invite IRS scrutiny, and too high means unnecessary payroll taxes. Beyond salary, mid-year is a good time to look at any major purchases or investments you’re planning for the second half of the year. Equipment, vehicles, real estate, and even hiring decisions can all carry meaningful tax implications, and timing them thoughtfully, rather than rushing at year-end, gives you more control over the outcome.

5. Use This Moment to Look at the Bigger Picture

Tax planning doesn’t exist in a vacuum. The best mid-year check-ins aren’t just about shaving dollars off your April bill. They’re about making sure your overall financial plan is still working the way it should. Have there been changes in your family, your business, or your goals since you last sat down with your advisor? Are there accounts or assets that aren’t currently part of your plan that could be better coordinated? A proactive conversation now, before the year gets away from you, is almost always more productive than a reactive one in January. The goal isn’t just to minimize taxes this year. It’s to make sure every part of your financial life is moving in the same direction.

As always, thank you for reading.

Kevin Dodgson CPA, CFA, CFP®

Founder & CEO, Shetland Financial